NSE: KIRLOSENG | BSE: 533293 | Sector: Capital Goods — Diesel Engines & Gensets

Rating: BUY | 6M Target: ₹1,720 | 12M Target: ₹2,050 | Date: February 2026

Investment Snapshot

| Parameter | Value | Parameter | Value |

| Current Price | ₹1,438 | Market Cap | ~₹20,500 Cr |

| 52-Week High | ₹1,434.90 (Feb 11, 2026) | 52-Week Low | ₹544.40 (Feb 28, 2025) |

| P/E Ratio (TTM) | ~38x (Standalone) | P/B Ratio | ~6.1x |

| ROCE | ~22% | ROE | ~15.6% |

| Net Cash Position | ₹448 Cr (FY25) | FY25 Revenue (Consol.) | ₹7,334 Cr |

| FY25 PAT (Consol.) | ₹534 Cr | FY25 PAT (Standalone) | ₹449 Cr |

| Dividend (FY26 Interim) | ₹2.50/share | Payout Record Date | Feb 20, 2026 |

| 6M Target | ₹1,720 | 12M Target | ₹2,050 |

Rating and Price Targets

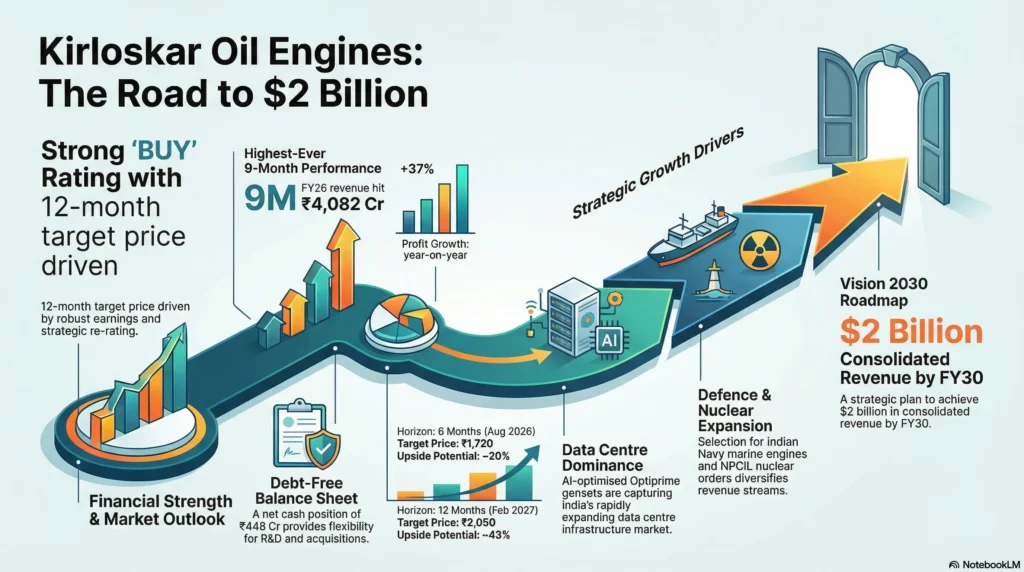

We initiate coverage on Kirloskar Oil Engines Limited (KOEL) with a BUY rating. The company has just delivered its highest-ever 9-month standalone performance (9M FY26: ₹4,082 Cr revenue, ₹330 Cr PAT) and is firing on all cylinders across B2B, industrial, defence, and international segments. Trading at ~38x TTM earnings with a credible $2 billion Vision 2030 roadmap in motion, we see significant upside from current levels.

| Horizon | Target Price | Upside Potential | Rating | Key Catalyst |

| 6 Months (Aug 2026) | ₹1,720 | ~20% | BUY | Q4 FY26 earnings, data centre ramp, NPCIL orders |

| 12 Months (Feb 2027) | ₹2,050 | ~43% | BUY | Vision 2030 execution, defence scale-up, Arka retail expansion |

Company Overview

Kirloskar Oil Engines Limited (KOEL) is the flagship engineering company of the Kirloskar Group, one of India’s most storied industrial conglomerates. Incorporated in 1946 and headquartered in Pune, Maharashtra, KOEL is one of the world’s largest manufacturers of diesel and gas engines and generating sets, with an 80-year track record of engineering excellence. Its products power critical infrastructure across agriculture, power generation, construction, railways, marine, defence, and data centres.

The company operates four state-of-the-art manufacturing plants at Kagal, Pune, Nashik, and Rajkot, and has a global presence spanning 70+ countries, with offices in Dubai (Middle East), South Africa, Kenya (Africa), and Houston (USA). With a strong network of dealers and service centres across India and abroad, KOEL commands ~24% volume market share in domestic diesel generator sets.

Business Segments

- B2B — Power Generation: Diesel and gas gensets from 5 kVA to 12,000 kVA (including Ultra-High Horse Power for data centres). Flagship products include Sentinel Series, Optiprime Series (AI/data centre-optimised), and KOEL Green range.

- B2B — Industrial: Engines for construction equipment, railways, marine, defence, and agricultural machinery. Selected by Indian Navy for 6 MW Medium-Speed Marine Diesel Engine development.

- B2B — International: Revenue-generating presence across Middle East, Africa, and North America. Revenue growing at 39% YoY in Q3 FY26.

- B2B — Aftermarket: Spares, services, and maintenance. Growing at 19% YoY — high-margin, recurring revenue stream.

- B2C — Fluid Dynamics (La-Gajjar Machineries): Pumps, tillers, agri equipment — transferred to wholly owned subsidiary via slump sale in Oct 2025 for dedicated focus.

- Arka Fincap (NBFC Subsidiary): 100%-owned NBFC offering corporate, MSME, and real estate loans. Building out retail secured lending — 85 new branches opened in 9M FY26, ₹328 Cr disbursed in retail secured lending.

Vision 2030 — $2 Billion Enterprise

Under the leadership of Managing Director Gauri Kirloskar, KOEL has articulated a bold Vision 2030: to grow into a $2 billion (approximately ₹17,000 Cr consolidated revenue) enterprise by FY30. This implies a 5-year revenue CAGR of approximately 15% from FY25 levels. The roadmap is phased: FY26 focuses on B2B manufacturing optimization; FY27 on technology roadmap and Arka retail growth; FY28 on inorganic expansion and international markets; FY29 on defence/rail diversification; and FY30 on full portfolio integration. At the end of the 2x3y plan (FY22-FY25), KOEL delivered revenue growth of 1.6x, EBITDA growth of 2.4x, and cash from operations growth of 2.6x — demonstrating management’s execution credibility.

Financial Analysis

Annual Revenue & Profitability (₹ Crores, Standalone)

| Metric | FY21 | FY22 | FY23 | FY24 | FY25 | FY26E (TTM) |

| Revenue (₹ Cr) | ~2,900 | ~3,200 | ~4,500 | ~4,785 | 5,073 | ~5,500+ |

| EBITDA (₹ Cr) | ~290 | ~384 | ~540 | ~573 | ~622 | ~730+ |

| EBITDA Margin | ~10% | ~12% | ~12% | ~12% | ~12.3% | ~13%+ |

| Net Profit (₹ Cr) | ~143 | ~221 | ~374 | ~451 | ~449 | ~460+ |

| EPS (₹) | ~10 | ~15 | ~26 | ~31 | ~31.5 | ~33-40 |

Consolidated Annual Performance (₹ Crores)

| Metric | FY24 | FY25 | 9M FY26 | FY26E |

| Revenue (₹ Cr) | ~6,800 | 7,334 | 5,585 | ~7,800+ |

| EBITDA (₹ Cr) | ~850 | ~980 | ~1,040 (9M) | ~1,380+ |

| Net Profit (₹ Cr) | ~530 | 534 | ~402 (9M) | ~550+ |

| EPS (₹) | ~37 | ~37.5 | ~28.2 (9M) | ~39-42 |

Quarterly Standalone Performance (₹ Crores)

| Quarter | Revenue | EBITDA | EBITDA Margin | PAT | EPS (₹) |

| Q4 FY25 (Mar 2025) | 1,401 | 171 | 12.1% | 106 | 7.40 |

| Q1 FY26 (Jun 2025) | 1,434 | 187 | 13.0% | 158 | 11.10 |

| Q2 FY26 (Sep 2025) | 1,598 | 214 | 13.4% | 163 | 11.44 |

| Q3 FY26 (Dec 2025) | 1,371 | 169 | 12.2% | 102 | 7.16 |

| 9M FY26 Total | 4,082 | 544 | 13.2% | 330 | 23.15 |

Note: Q3 FY26 showed seasonal softness due to the B2C restructuring and post-CPCB4 demand normalization. However, year-to-date standalone PAT of ₹330 Cr is 37% ahead of the prior year — a strong underlying growth trajectory. Q2 FY26 was the company’s best-ever quarter, crossing the ₹1,500 Cr revenue milestone for the first time.

Segment Revenue Breakdown (Q3 FY26 YoY, Consolidated)

| Segment | Q3 FY26 Revenue | YoY Growth | Commentary |

| B2B – Power Generation | ₹1,396 Cr (segment) | 35.9% | Volume growth + HHP/data centre mix shift |

| B2B – B2C (Fluid Dynamics) | ₹249 Cr | 18.4% | Post-restructuring — now in subsidiary |

| Financial Services (Arka) | ₹227 Cr | 7.3% | Building retail secured book |

| Total Consolidated | ₹1,873 Cr | 29.2% | Broad-based growth; highest-ever Q3 |

Key Financial Ratios & Valuation

| Ratio | Value | Commentary |

| P/E (TTM Standalone) | ~38-42x | Premium vs peers; justified by growth momentum & Vision 2030 |

| P/E (Consolidated) | ~37x | Lower on consolidated — Arka creates hidden value |

| P/B Ratio | ~6.1x | Reflects strong brand equity and ROCE |

| ROCE | ~22% | Healthy capital efficiency |

| ROE | ~15.6% | Conservative leverage; improving with scale |

| Net Cash | ₹448 Cr (FY25) | Zero net debt — strong balance sheet |

| Dividend Yield | ~0.7% | FY26 interim: ₹2.50/share (₹20 face → wait, FV ₹2) |

| 52-Wk Return | ~164% | From ₹544 low to ₹1,438 — massive re-rating underway |

| Revenue CAGR (3Y) | ~16-18% | FY22-FY25 standalone CAGR |

| EBITDA CAGR (3Y) | ~17% | Margins stable at 12-13%; expansion potential ahead |

Investment Thesis

Bull Case — Why BUY?

- Record-Breaking Momentum: KOEL delivered its highest-ever Q1 (₹1,434 Cr), Q2 (₹1,598 Cr), and Q3 standalone revenues in FY26, with 25% year-to-date growth — demonstrating broad-based demand acceleration across all segments.

- Data Centre Megatrend: The Optiprime series of ultra-high-horsepower gensets (for AI data centres requiring 5kVA-12,000kVA uninterrupted power) has received strong market acceptance. India’s data centre capacity is expected to triple by 2028 — KOEL is the domestic leader in this space.

- Defence — Structural New Driver: KOEL was selected by the Indian Navy to develop a 6MW Medium-Speed Marine Diesel Engine — a flagship Atmanirbhar Bharat achievement. NPCIL nuclear power orders expected to start contributing revenue from FY27.

- $2 Billion Vision 2030: Management has a credible track record (2x3y plan delivered 2.4x EBITDA growth). With ₹7,334 Cr consolidated FY25 revenue, reaching ₹17,000 Cr by FY30 requires ~15% CAGR — well within reach given current momentum.

- B2C Restructuring Unlocks Value: Transferring the B2C segment (pumps/agri) to La-Gajjar Machineries allows focused management bandwidth on the high-growth B2B and industrial segments, improving capital efficiency.

- Arka Fincap Hidden Value: NBFC with 85 new branches in 9M FY26, growing secured retail book. As Arka scales, its separate valuation could provide a significant sum-of-the-parts re-rating for KOEL’s consolidated equity.

- Strong Net Cash Position: ₹448 Cr net cash with no debt — gives flexibility for capex, R&D investments, and potential acquisitions aligned with Vision 2030.

- 52-Week Rally Validates Re-Rating: The stock has already surged ~164% from its one-year low of ₹544, but with continued earnings delivery and multiple re-rating catalysts ahead, the story is far from over.

Bear Case — Key Risks

- Valuation Premium Risk: At ~38-42x standalone P/E, KOEL trades at a significant premium. Any earnings miss or guidance cut could trigger a sharp correction. Investors should monitor EBITDA margin trends closely.

- Post-CPCB4 Demand Normalization: The CPCB4+ emission norm transition caused a demand pullback in gensets in FY25. While demand is recovering, any renewed slowdown in industrial/construction capex could impact near-term revenues.

- Promoter Stake Decline: Promoter holding has decreased by 18.3% over the last 3 years (now at 41.1%). This is a notable concern and has historically weighed on the stock’s valuation.

- Arka Fincap Execution Risk: The NBFC business is still in early retail expansion. Any credit quality deterioration or macroeconomic stress in MSME/real estate lending could negatively impact KOEL’s consolidated financials.

- B2C Integration Disruption: The slump sale of B2C operations to La-Gajjar Machineries caused near-term production disruption (noted in Q3 FY25 results). Full integration benefits may take 2-3 quarters to materialize.

- Currency Risk: With 70+ country presence and growing international revenues, KOEL faces forex exposure in USD/EUR-denominated contracts, particularly in Middle East and Africa.

- Competition from Global Players: Cummins India (listed, ~30-40x P/E), Greaves Cotton, and Caterpillar remain formidable competitors in large genset and industrial engine segments.

Technical Outlook

6-Month Technical View

Kirloskar Oil Engines has staged a remarkable recovery from its 52-week low of ₹544 (February 2025) to hit a fresh 52-week high of ₹1,434.90 on February 11, 2026 — driven by its Q3 FY26 results. The stock is currently in a strong uptrend with all moving averages aligned bullishly. Key technical levels:

| Level | Price (₹) | Significance |

| Strong Support | ₹1,250 – ₹1,300 | Previous breakout zone; golden pocket for SIP |

| Immediate Support | ₹1,380 – ₹1,400 | Recent consolidation; add on dips |

| Current Zone | ₹1,420 – ₹1,450 | 52-week high zone; breakout in progress |

| Immediate Target | ₹1,600 – ₹1,650 | Next resistance from 2023 highs |

| 6M Target | ₹1,720 | ~20% upside; P/E-based + technical |

| 12M Target | ₹2,050 | ~43% upside; Vision 2030 re-rating |

| Stop Loss | ₹1,200 | For swing traders; below 200-DMA |

Technically, a sustained breakout above ₹1,435 (52-week high) on strong volume would be a very bullish signal, opening up price discovery towards ₹1,700+. The stock has strong momentum with RSI in the 60-70 range and MACD positive.

Sector & Macro Context

India’s power infrastructure, data centre, construction, and defence sectors are all simultaneously growing — creating a perfect demand environment for KOEL’s products. The government’s ₹11+ lakh crore capital expenditure budget in FY25, the PLI schemes for manufacturing, and the 100+ GW renewable energy push (requiring backup diesel gensets during transition) all support demand for KOEL’s core products.

The data centre boom is a particularly exciting structural tailwind. India’s AI-driven data centre construction cycle is accelerating, with over ₹2 lakh crore of announced investments from Reliance, Adani, Google, Microsoft, and Amazon. Each data centre requires multiple high-capacity gensets (often 1,000 kVA to 12,000 kVA) for backup power — directly in KOEL’s Optiprime wheelhouse.

In defence, India’s indigenization drive (Atmanirbhar Bharat) mandates local procurement for military equipment. KOEL’s selection by the Indian Navy for marine engine development and its growing exposure to railways/NPCIL nuclear orders positions it uniquely in this high-value segment.

Peer comparison: Cummins India (~₹52,000 Cr market cap, P/E ~45x) and Greaves Cotton (~₹4,000 Cr market cap) are the closest domestic comparables. KOEL trades at a meaningful discount to Cummins on market cap (₹20,500 Cr vs ₹52,000 Cr) despite superior growth momentum and a broader product portfolio, suggesting further re-rating potential.

Key Catalysts to Watch

| Catalyst | Timeline | Potential Impact |

| Q4 FY26 Earnings & FY26 Full-Year Results | Apr-May 2026 | Full-year PAT above ₹460 Cr standalone = positive trigger |

| NPCIL Nuclear Power Orders Revenue | FY27 onwards | High-value, recurring government revenues |

| Indian Navy Marine Engine Milestones | FY26-27 | Defence revenue diversification — significant re-rating catalyst |

| Data Centre Optiprime Order Wins | Ongoing | Validates HHP strategy; high ASP = margin accretive |

| Arka Fincap Retail Book Scaling | FY26-27 | ₹1,000+ Cr disbursed → NBFC valuation unlock |

| Promoter Stake Stabilization | FY26 | Positive signal if promoter buying resumes |

| La-Gajjar B2C Integration Benefits | FY26-27 | Cost savings + dedicated B2C growth = profitability improvement |

| International Business Acceleration | Ongoing | Middle East & Africa market deepening → export premium |

Valuation & Target Price Derivation

6-Month Target Price: ₹1,720

We apply a P/E of ~43x on estimated FY26 standalone EPS of approximately ₹40 (based on 9M PAT of ₹330 Cr + expected Q4 ~₹115-120 Cr = ~₹445-450 Cr FY26 PAT / 14.3 Cr shares = ₹31-32 standalone). On consolidated basis with Arka contribution, blended EPS is higher. Factoring in P/E expansion to 43x on FY26 standalone EPS of ₹40, we arrive at ₹1,720 for the 6-month target.

12-Month Target Price: ₹2,050

For the 12-month target, we estimate FY27 consolidated PAT of approximately ₹680-700 Cr (incorporating: 15% revenue growth to ~₹8,500 Cr, EBITDA margin expansion to ~13.5%, and Arka’s growing contribution). On a P/E of ~42x FY27E standalone EPS of ~₹49-50, and adding Arka subsidiary value (sum-of-the-parts), we derive a 12-month target of ₹2,050, representing ~43% upside.

Risk Matrix

| Risk Factor | Severity | Likelihood | Mitigation |

| Valuation De-rating | High | Low-Med | Consistent earnings delivery at 25%+ PAT growth |

| CPCB4+ Demand Normalization | Medium | Medium | Diversified segments (defence/data centre) offset |

| Promoter Stake Decline | Medium | Medium | Watch disclosures; institutional buying counterbalances |

| Arka Credit Quality Risk | Medium | Low | Secured retail focus; conservative lending norms |

| B2C Integration Disruption | Low-Med | Low (ongoing) | Mostly behind; benefits to flow from FY27 |

| Forex Volatility | Low | Medium | Partial natural hedge via import-linked pricing |

| Competition — Cummins India | Medium | Ongoing | KOEL’s multi-segment diversification is a key moat |

Recommendation Summary

BUY | 6-Month Target: ₹1,720 | 12-Month Target: ₹2,050

Kirloskar Oil Engines Limited stands at an inflection point — transitioning from a traditional genset manufacturer to a multi-segment energy solutions enterprise with exposure to India’s most exciting structural growth themes: data centres, defence indigenization, nuclear energy, and global export markets. The company’s Vision 2030 roadmap ($2 billion revenue by FY30) has strong management credibility behind it after the 2x3y plan delivered 2.4x EBITDA growth.

With record-breaking quarterly revenues in FY26, a net cash balance sheet, growing international presence, and transformative strategic initiatives underway, KOEL is a high-conviction BUY. We recommend investors accumulate in the ₹1,350-1,450 range on any dips, with a 12-18 month view towards ₹2,050+.

DISCLAIMER

This report is for informational and educational purposes only. It does not constitute investment advice or a solicitation to buy or sell securities. Past performance is not indicative of future results. Investors should conduct their own due diligence and consult a registered financial advisor before making investment decisions. All data is sourced from publicly available information and is subject to change.