Ramesh had been working as a credit officer at a mid-sized public sector bank in Nagpur for six years. He had processed hundreds of loan files, sat through countless branch meetings, and still — when the question on NPA classification appeared in his promotion exam — he blanked out. He knew what NPA meant in everyday conversation, but the precise definitions, timelines, and provisioning requirements had always felt like abstract regulation-speak rather than something grounded in real branch life.

If that story sounds familiar, you are in exactly the right place.

NPA classification — the formal process by which banks categorize Non-Performing Assets as Substandard, Doubtful, or Loss Assets — is one of the most consistently tested topics in IBPS PO, SBI PO, RBI Grade B, and internal bank promotion examinations. Yet it is also one of the most poorly understood, largely because most study material presents it as dry regulatory text stripped of any real-world context.

This guide changes that. We will walk through everything you need to know about NPA classification — the definitions, the RBI guidelines, the provisioning norms, real branch examples, common exam question patterns, and practical memory hooks — all in plain language that actually sticks.

1. What Is NPA? The Foundation You Cannot Skip

Before diving into NPA classification, let us make sure the foundation is solid. NPA stands for Non-Performing Asset. In the context of Indian banking, an asset is essentially a loan or advance extended by a bank. The moment that loan stops generating income for the bank — because the borrower is not making repayments — it becomes non-performing.

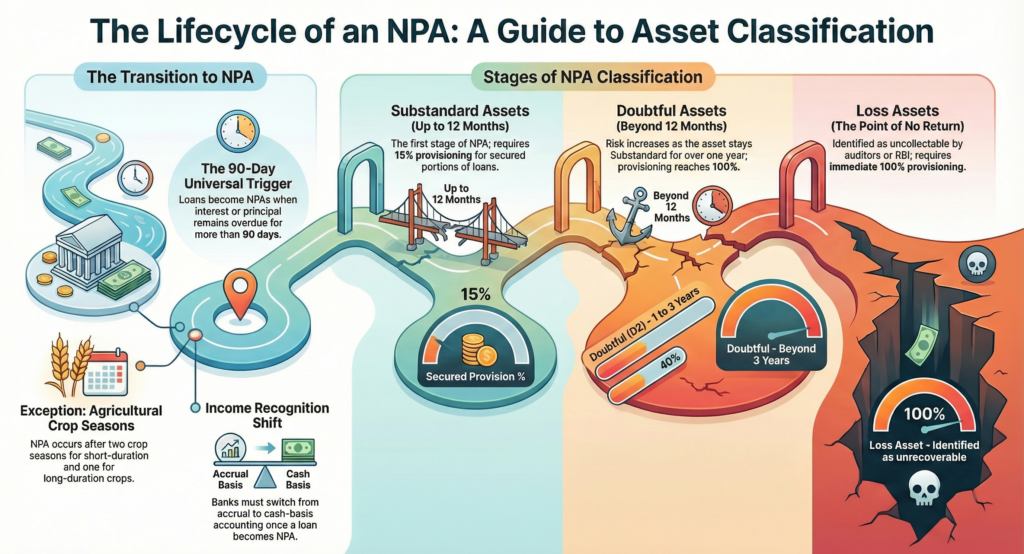

The Reserve Bank of India defines a Non-Performing Asset as a loan or advance where interest or principal installment remains overdue for a period of more than 90 days. This is the famous 90-day norm, and it is the single most important number in the entire NPA framework.

📌 RBI Definition: As per RBI’s Prudential Norms on Income Recognition, Asset Classification and Provisioning (IRAC Norms): ‘A non-performing asset (NPA) is a loan or an advance where (i) interest and/or installment of principal remains overdue for a period of more than 90 days in respect of a term loan.’

Prior to 2004, banks used a 180-day norm. The shift to 90 days was part of RBI’s effort to align Indian banking standards with international best practices. Today, 90 days is the universal benchmark — and any exam question about the NPA trigger period has one correct answer: 90 days.

Special Cases: When the 90-Day Rule Has Exceptions

Not every loan type follows the standard 90-day calendar. Here are the key exceptions that frequently appear in exams:

- Agricultural loans (short-duration crops): If interest or principal is not paid within two crop seasons from the due date.

- Agricultural loans (long-duration crops): If interest or principal is not paid within one crop season from the due date.

- Overdraft and cash credit accounts: Classified as NPA if the account remains out of order for 90 days. An account is ‘out of order’ if the outstanding balance exceeds the sanctioned limit for 90 consecutive days, or if no credits are received for 90 days.

- Bills purchased and discounted: Classified as NPA if the bill remains overdue for 90 days.

✅ Pro Tip: The agricultural NPA exception is a favourite in both IBPS PO and JAIIB/CAIIB exams. Learn both crop durations — short (two seasons) and long (one season) — and you will never miss this sub-question.

2. The Three Types of NPA Classification: A Deep Dive

Once a loan becomes NPA, it does not stay in a single category forever. As time passes and recovery becomes less likely, the asset is classified into progressively worse categories. RBI prescribes three formal categories under NPA classification, and understanding each one — its definition, timeline, and provisioning requirement — is essential for every banking exam.

| NPA Category | Definition / Timeline | Provisioning Required | Risk Level |

| Substandard Asset | NPA for up to 12 months | 15% (secured); 25% (unsecured) | Moderate Risk |

| Doubtful Asset | Substandard for more than 12 months | 25% to 100% (based on age) | High Risk |

| Loss Asset | Identified as uncollectible by bank/auditor/RBI inspector | 100% | Extremely High Risk |

2.1 Substandard Asset — The First Stage of NPA

A Substandard Asset is a loan that has remained NPA for a period of up to 12 months. In simple terms: if today is Day 91 after the loan went past its due date (making it NPA), it enters the Substandard category. It stays there until it has been NPA for 12 months.

At this stage, the bank still has some hope of recovery. The borrower may be facing temporary financial difficulty — a business slowdown, a medical emergency, a crop failure — but the underlying asset (if any collateral exists) may still retain value.

The provisioning requirement for Substandard Assets is 15% of the outstanding amount for secured loans, and 25% for unsecured loans. This means the bank must set aside that percentage of the loan amount as a provision in its accounts, reducing reported profits accordingly.

📋 Real-Life Example: Suresh runs a small garment export business in Surat. He had a working capital loan of Rs. 20 lakh from a nationalized bank. Due to a cancellation of overseas orders during the pandemic, he stopped repaying in March 2023. By June 2023 (90 days later), the account became NPA. As of June 2024 — 12 months later — the account is still classified as Substandard, and the bank has made a provision of Rs. 3 lakh (15% of Rs. 20 lakh) in its books.

2.2 Doubtful Asset — Recovery Becomes Uncertain

A Doubtful Asset is one that has remained in the Substandard category for more than 12 months. The name itself tells you everything about how the bank views these loans — recovery is now genuinely doubtful.

At this point, the collateral may have depreciated, the borrower’s financial situation has deteriorated further, and legal recovery proceedings may have begun. Provisioning requirements for Doubtful Assets are more stringent and are tiered based on how long the asset has been doubtful:

| Period in Doubtful Category | Secured Portion | Unsecured Portion |

| Up to 1 year (D1) | 25% | 100% |

| 1 to 3 years (D2) | 40% | 100% |

| More than 3 years (D3) | 100% | 100% |

Notice that the unsecured portion is always provisioned at 100% — because without collateral, the bank has nothing to recover against. For the secured portion, provisioning escalates from 25% to 100% over three years, reflecting the progressive erosion of asset value.

📋 Real-Life Example: Continuing with Suresh’s account from above: by June 2025 (24 months into NPA, 12 months into Doubtful), his account is now classified as D2 — Doubtful for 1 to 3 years. The bank has filed a case before the Debt Recovery Tribunal. The provisioning requirement has increased to 40% of the secured outstanding amount, plus 100% of any unsecured component. The bank’s provision charge in its P&L account increases significantly.

2.3 Loss Asset — The Point of No Return

A Loss Asset is a loan that has been identified as uncollectible and of such little value that its continuance as a bankable asset is not warranted. It is not necessarily written off immediately, but the bank has fully acknowledged that recovery is not expected.

Importantly, a Loss Asset is identified not just by the bank itself but can be flagged by the bank’s statutory auditors or by inspectors from the RBI during their supervisory review. The requirement for outside identification distinguishes this category from the earlier two.

Provisioning for Loss Assets is 100% — meaning the bank must set aside the full outstanding amount as a provision. The loan still exists in the books until it is technically written off, but the bank has already absorbed the full loss in its profit and loss account.

⚠️ Important: A common exam trap: students confuse ‘Loss Asset’ with ‘Written-Off Account’. They are not the same. A Loss Asset is provisioned at 100% but still technically on the books. A written-off account has been removed from the bank’s balance sheet entirely. Writing off an account does not mean the bank stops pursuing recovery — legal efforts may continue.

3. The NPA Classification Timeline: A Visual Walkthrough

One of the most confusing aspects of NPA classification for exam aspirants is getting the timelines exactly right. Let us trace a single loan from sanction to Loss Asset status step by step.

| Milestone | What Happens | Classification | Provisioning |

| Day 0 | EMI/interest due date passes unpaid | Standard Asset | 0.25% – 0.40% |

| Day 91 | 91st day of non-payment | NPA (triggers) | — |

| Day 91 – Month 12 | Within first 12 months as NPA | Substandard Asset | 15% / 25% |

| Month 13 onwards | More than 12 months as NPA | Doubtful Asset (D1) | 25% / 100% |

| After 3 more years | More than 3 years as Doubtful | Doubtful Asset (D3) | 100% / 100% |

| When identified as unrecoverable | Bank/Auditor/RBI flags as loss | Loss Asset | 100% |

✅ Pro Tip: Print this timeline and stick it near your study desk. NPA classification is almost always tested as a sequencing problem — ‘After how many months does a Substandard Asset become Doubtful?’ Answer: 12 months as NPA (not from loan sanction date). The starting clock is the NPA date, not the loan date.

4. Income Recognition: The Rule That Changes How Banks Report Profits

NPA classification does not just affect how loans are categorized on the balance sheet — it fundamentally changes how a bank records income from those loans. This is called the Income Recognition principle, and it is part of the broader IRAC norms issued by the RBI.

For a Standard Asset (a performing loan), the bank records interest income on an accrual basis — meaning it records the interest income as earned, even if the borrower has not yet paid it. This is normal accounting practice.

However, the moment a loan is classified as NPA, the bank must switch to a cash basis for income recognition. This means the bank can only record interest income when the cash is actually received. Any previously accrued but unpaid interest must be reversed from income books.

📋 Real-Life Example: Consider a term loan of Rs. 50 lakh with an annual interest rate of 10%. In a typical month, the bank would accrue Rs. 41,667 in interest income even if not yet received. Once the account becomes NPA, those accruals stop. If the bank had already booked Rs. 2.5 lakh of interest income for the year from this account and the loan then became NPA, that Rs. 2.5 lakh must be reversed — wiping it from the income statement. This is why NPA directly hits bank profitability, not just in provisioning but in revenue recognition.

This income reversal is a major reason why banks are extremely cautious about NPA slippage — the simultaneous loss of income recognition and the requirement to make provisions creates a double hit on the profit and loss account.

📊 Key Exam Point: Income recognition on NPA accounts shifts from accrual basis to cash basis. This means a bank CANNOT book interest income on an NPA loan unless it is actually received. Questions on this principle appear regularly in JAIIB Paper 2 (Accounting & Finance for Bankers) and promotion tests.

5. Provisioning Norms: What Banks Must Set Aside and Why

Provisioning is the process by which a bank sets aside a portion of its profits as a cushion against potential loan losses. Think of it as a bank’s internal insurance system — it reduces reported profits in the short term to protect against larger losses in the future.

RBI’s provisioning norms are mandatory and non-negotiable. Banks cannot choose whether to make provisions — they are required to do so as part of prudential regulation. Let us look at the complete provisioning matrix:

| Asset Category | Sub-category | Secured Loan | Unsecured Loan |

| Standard Asset | — | 0.25% (term loan) | 0.25% |

| Substandard Asset | Up to 12 months NPA | 15% | 25% |

| Doubtful – D1 | Up to 1 year as Doubtful | 25% | 100% |

| Doubtful – D2 | 1 to 3 years as Doubtful | 40% | 100% |

| Doubtful – D3 | More than 3 years as Doubtful | 100% | 100% |

| Loss Asset | Identified as unrecoverable | 100% | 100% |

The economic logic behind escalating provisioning is straightforward: as time passes, the probability of recovering the loan decreases, so the bank must acknowledge a progressively larger potential loss on its books. This builds financial resilience and prevents the kind of balance sheet shock that has historically triggered banking crises globally.

6. A Real Branch Story: How NPA Classification Plays Out on the Ground

Theoretical knowledge is one thing; understanding how it applies at the branch level is what separates good candidates from great ones — especially in promotion tests where case-based questions are common.

Let us follow one account from sanction to write-off through a realistic scenario.

The Story of Mehta Traders

Mr. Arvind Mehta is a wholesale cloth merchant in Indore who had been a loyal customer of National Co-operative Bank for 14 years. In 2021, he availed a cash credit limit of Rs. 40 lakh against hypothecation of stock. For two years, the account ran smoothly — regular turnover, timely interest payments, and occasional excess allowed.

Then in mid-2023, a large consignment was rejected by a buyer, leading to a cash flow crisis. Mehta stopped servicing the account. Here is how the account progressed through NPA classification:

| Date | Event | Classification | Bank Action |

| July 2023 | Last credit in the CC account; account goes out of order | Standard Asset | Relationship Manager visits Mehta |

| October 2023 | 90 days out of order — account becomes NPA | Substandard Asset | Income recognition stopped; provision of 15% made |

| October 2024 | 12 months as NPA completed | Doubtful (D1) | SARFAESI notice issued; provision increased to 25% |

| October 2025 | More than 1 year as Doubtful | Doubtful (D2) | DRT case filed; provision increased to 40% |

| 2026 onwards | Auditors certify as unrecoverable (collateral eroded) | Loss Asset | 100% provision made; write-off process initiated |

Notice what happened at each stage: the bank did not sit idle. From relationship management to SARFAESI notices to DRT proceedings, recovery efforts ran in parallel with the classification progression. This is exactly the kind of branch-level understanding that impresses promotion test evaluators who are often senior bankers themselves.

7. Why NPA Matters: The Bigger Picture for Banks and the Economy

Understanding NPA classification is not just about clearing exams. It is about understanding why the entire Indian banking sector — and by extension, the economy — is deeply affected by the quality of bank loan portfolios.

Impact on Bank Profitability

NPAs affect a bank’s profits in two simultaneous ways. First, through lost income — the bank cannot book interest income on NPA accounts, so revenue falls. Second, through mandatory provisioning — a portion of profits must be set aside as provisions, directly reducing net profit. In extreme cases, a high NPA portfolio can push a bank into losses even if its other operations are profitable.

Impact on Capital Adequacy

Under Basel III norms (which India follows), banks must maintain a minimum Capital Adequacy Ratio (CAR) of 11.5% for Indian public sector banks. Higher NPAs require higher provisioning, which erodes the capital base, potentially pushing a bank below the minimum CAR threshold. The result: RBI may impose the Prompt Corrective Action (PCA) framework — restricting the bank’s ability to lend, expand, or declare dividends.

Impact on Lending and the Economy

When a bank is burdened with high NPAs, it becomes risk-averse. It tightens lending standards, approves fewer loans, and focuses on recovery rather than expansion. This contraction in credit supply has downstream effects on businesses, employment, and economic growth — particularly in sectors like MSME, agriculture, and infrastructure that depend heavily on bank credit.

📈 Did You Know: India’s Gross NPA ratio for Scheduled Commercial Banks peaked at 11.5% in March 2018 following the Asset Quality Review (AQR) launched by RBI in 2015-16. Since then, significant improvements through the Insolvency and Bankruptcy Code (IBC), SARFAESI enforcement, and write-offs have brought it down to around 3.2% by March 2024 — the lowest in over a decade.

8. Recovery Tools Available to Banks: From NPA to Resolution

A common misconception is that once a loan becomes NPA, the money is lost. In reality, banks have a robust legal and administrative toolkit for recovering dues. Understanding these tools is important for both exams and for banking professionals at the branch level.

SARFAESI Act, 2002

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, commonly called SARFAESI, allows banks to recover NPAs without court intervention by taking possession of secured assets. A bank can invoke SARFAESI once the loan has been NPA for more than 60 days (and a formal notice has been issued). This is the most powerful and widely used recovery tool for secured loans above Rs. 1 lakh.

Debt Recovery Tribunals (DRT)

DRTs were established under the Recovery of Debts Due to Banks and Financial Institutions (RDDBFI) Act, 1993. Banks can file an Original Application (OA) at the DRT for recovery of dues above Rs. 20 lakh. DRT proceedings are faster than civil courts but can still take 1–3 years.

Lok Adalats

For smaller NPAs — typically up to Rs. 20 lakh — banks can use Lok Adalats for out-of-court settlements. This is especially useful for agricultural and retail NPAs where borrowers may be willing to negotiate but cannot afford litigation.

Insolvency and Bankruptcy Code (IBC), 2016

The IBC introduced a time-bound insolvency resolution process for corporate borrowers, typically 180–330 days. It represents the most significant structural reform in NPA resolution since liberalization. Banks can initiate Corporate Insolvency Resolution Process (CIRP) against defaulting corporate borrowers with dues above Rs. 1 crore.

One-Time Settlement (OTS)

Banks can offer OTS schemes to borrowers — allowing them to settle outstanding dues at a negotiated amount lower than the total outstanding, in exchange for full and final settlement. This is commonly used for smaller and mid-sized NPAs where litigation costs would outweigh recovery.

✅ Pro Tip: In promotion exams, questions on SARFAESI frequently appear. Remember: SARFAESI applies only to secured loans, not to unsecured personal loans, agricultural loans (in some cases), or loans below Rs. 1 lakh. These exceptions are commonly tested.

9. Exam-Focused: Most Commonly Asked Questions on NPA Classification

Let us look at the types of questions that regularly appear in bank exams and promotion tests related to NPA classification. Understanding the question patterns is as important as knowing the content.

Pattern 1: Definition-Based Questions

‘When is a loan classified as NPA?’ The answer must be precise: when interest or principal installment remains overdue for more than 90 days (with crop-based exceptions for agriculture).

Pattern 2: Timeline and Classification

‘An account became NPA on 1st April 2022. On 1st May 2023, how should it be classified?’ — It has been NPA for 13 months, which means it crossed 12 months in April 2023. As of May 2023, it is a Doubtful Asset (D1).

Pattern 3: Provisioning Calculations

‘A secured term loan of Rs. 10 lakh has been Doubtful (D2) for 2 years. What is the provision required?’ — D2 requires 40% provision on the secured portion. 40% of Rs. 10 lakh = Rs. 4 lakh.

Pattern 4: Income Recognition

‘A bank has been accruing Rs. 50,000 per month as interest income on a term loan. The loan becomes NPA. What happens to previously accrued income?’ — It must be reversed. The bank can only recognize interest income on this account when cash is actually received.

Pattern 5: Upgrade of NPA

‘Can an NPA account be upgraded to Standard Asset?’ — Yes. If all arrears of interest and principal are fully paid, the account can be upgraded to Standard. However, it must demonstrate sustained satisfactory performance for at least one repayment cycle before being upgraded.

🎯 High-Value Exam Insight: In JAIIB Paper 1 (Principles & Practices of Banking) and internal promotion tests, the ‘upgrade of NPA’ concept is increasingly tested. Many candidates incorrectly assume an NPA account stays NPA forever. It does not — repayment can restore its classification to Standard, though with conditions.

10. Quick Revision Card: Everything You Need in 5 Minutes

Short on time before the exam? Here is the condensed version of everything covered in this guide:

- NPA trigger: Interest or principal overdue for more than 90 days (term loans).

- Agriculture exceptions: Short-duration crops — 2 crop seasons; Long-duration crops — 1 crop season.

- Substandard Asset: NPA for up to 12 months. Provision: 15% (secured) / 25% (unsecured).

- Doubtful Asset: Substandard for more than 12 months. Tiered provisioning from 25% to 100%.

- Loss Asset: Identified as unrecoverable by bank / auditor / RBI inspector. Provision: 100%.

- Income recognition: Switches from accrual to cash basis on NPA classification. Prior accruals reversed.

- Standard Asset provisioning: 0.25% for most term loans (lower risk buffer).

- Upgrade possible: Full repayment of all arrears + one satisfactory repayment cycle.

- Recovery tools: SARFAESI (secured loans), DRT (> Rs. 20 lakh), IBC (> Rs. 1 crore corporate), Lok Adalat (< Rs. 20 lakh).

- NPA is not write-off: Loss Asset = 100% provisioned but still on books. Write-off = removed from balance sheet.

✅ Pro Tip: Create flashcards for the provisioning percentages. They are the most reliably tested numbers in this topic and the easiest to mix up under exam pressure.

Conclusion: From Regulatory Text to Real Understanding

NPA classification is one of those topics that can feel overwhelming when read as regulatory text, but becomes intuitive once you connect it to real branch situations. The progression from Standard Asset to Substandard to Doubtful to Loss is not a bureaucratic exercise — it is a bank’s honest accounting of the likelihood that a borrower will repay.

The 90-day norm, the three NPA categories, the provisioning matrix, the income recognition principles, and the recovery tools are not separate pieces of knowledge to be memorized in isolation. They form an interconnected system, and once you see that system clearly, the exam questions become logical rather than arbitrary.

Go back to Ramesh, our credit officer from Nagpur. Once he understood that Mehta Traders’ account — sitting on his desk right now, showing 95 days out of order — was already a Substandard Asset requiring immediate provisioning and income reversal, the regulation stopped being abstract. It was something he was already living. That realization is what the best exam preparation should produce.

Master NPA classification. Not just for the exam — for the banker you are becoming.

Tags: NPA classification, Non-Performing Asset, IBPS PO banking awareness, NPA types in banking, substandard doubtful loss asset, NPA provisioning norms, bank promotion exam preparation, IRAC norms RBI, 90-day NPA rule, JAIIB banking awareness

What is the full form of NPA in banking?

NPA stands for Non-Performing Asset. It refers to a loan or advance where repayment (interest or principal) is overdue for more than 90 days.

What is the 90-day rule in NPA?

As per RBI’s IRAC norms, any term loan where interest or principal installment is overdue for more than 90 continuous days is classified as a Non-Performing Asset. This is commonly called the ’90-day NPA norm’.

What are the three categories of NPA?

The three categories under NPA classification are: (1) Substandard Asset — NPA for up to 12 months, (2) Doubtful Asset — Substandard for more than 12 months, and (3) Loss Asset — identified as unrecoverable by the bank, auditor, or RBI.

What is the difference between Doubtful and Loss Asset?

A Doubtful Asset is one where recovery is considered unlikely but has not yet been formally identified as a loss. A Loss Asset is one that has been specifically identified as uncollectible by the bank itself, its auditors, or RBI inspectors. The key difference is the formal identification process — Loss Assets require explicit recognition by a qualifying authority.

Can an NPA be reversed to a Standard Asset?

Yes. An NPA account can be upgraded (‘regularized’) to Standard Asset status if all overdue interest and principal are paid in full. Additionally, the account should demonstrate sustained satisfactory performance for at least one repayment cycle before the upgrade is formalized in the bank’s books.

Why is NPA important in bank promotion exams?

NPA classification directly impacts a bank’s profitability, capital adequacy, and overall financial health. Bankers at all levels — from branch staff to senior managers — are expected to understand and apply IRAC norms in their day-to-day work. Promotion exams test this knowledge precisely because it is operationally critical, not merely academic.